The world of options trading holds a plethora of enigmatic terms that can confound even seasoned traders. Among these mystifying concepts, the “Greeks” stand out as cryptic figures, shrouding their true meaning in layers of Greek letters and mathematical complexities. But fear not, aspiring options enthusiasts! This exhaustive guide will embark on a journey through the Greek alphabet, unraveling the secrets of these enigmatic metrics and their profound impact on options trading strategies.

Image: www.youtube.com

Delving into the Greek Lexicon

The Greeks, a constellation of metrics, derive their name from the Greek letters assigned to them. These metrics quantify the intricate relationship between an option’s price and various factors that potentially influence its value. By mastering the intricacies of the Greeks, traders gain the ability to navigate the turbulent waters of options trading with enhanced precision and profitability.

Delta: The Anchor of Price Sensitivity

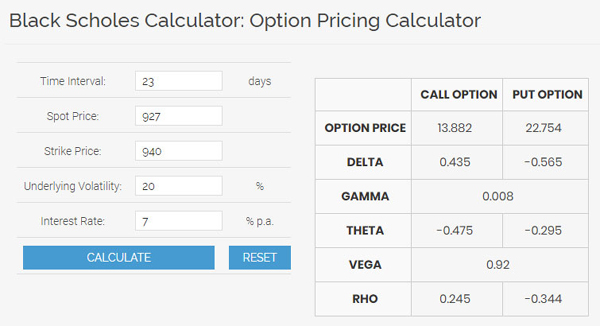

Delta, represented by the Greek letter Δ, serves as the cornerstone of the Greeks. It gauges the percentage change in an option’s price for every one-point movement in the underlying asset’s price. Delta values range between -1 and +1, indicating the sensitivity of an option’s value to the underlying asset’s fluctuations. Understanding Delta is crucial for predicting the impact of price movements and adjusting trading strategies accordingly.

Gamma: The Catalyst for Delta’s Change

Gamma, symbolized by the letter Γ, measures the rate at which Delta changes in response to a one-point shift in the underlying asset’s price. Gamma provides insight into the curvature of an option’s price-response curve, revealing whether Delta increases or decreases with price changes. This knowledge allows traders to fine-tune their strategies by identifying the points of maximum and minimum Delta sensitivity.

Image: www.youtube.com

Theta: The Time Terminator

Theta, represented by the Greek letter θ, embodies the relentless erosion of an option’s value as time passes. It measures the daily decay in option premiums attributed solely to the passage of time. Theta’s impact intensifies as options approach their expiration date, reminding traders of the fleeting nature of time value.

Vega: The Volatility Vicar

Vega, adorned with the Greek letter ν, captures the influence of implied volatility on an option’s price. Implied volatility, a gauge of the market’s expectations for future price swings, directly affects option pricing and Vega quantifies this relationship. Volatility-dependent strategies leverage Vega to exploit market volatility for potential gains.

Rho: The Interest Rate Intermediary

Rho, symbolized by the letter ρ, quantifies the impact of interest rate changes on option prices. Interest rates play a pivotal role in options pricing, particularly for long-term options, and Rho reveals the extent to which an option’s value adjusts with interest rate fluctuations.

What Do Greeks Mean In Options Trading

Image: bullbull.in

Conclusion

The Greeks, a formidable arsenal of metrics, bestow upon options traders an unparalleled understanding of options’ price dynamics. Comprehending the interplay between the Greeks and their underlying factors empowers traders to craft sophisticated trading strategies, calibrate risk exposure, and optimize profitability. Delve into this Greek alphabet of options trading, unlocking the secrets of price sensitivity, volatility assessment, and time decay. Knowledge is the key to conquering the complexities of options trading, and the Greeks hold the key, leading you towards informed decision-making and enhanced market prowess.