**

Image: www.benzinga.com

**

**

Introduction

In the dynamic world of options trading, beta serves as an indispensable metric that quantifies the relationship between an underlying asset and the broader market. Understanding how to calculate and interpret beta is crucial for both novice and seasoned options traders alike. By leveraging beta, traders can gauge the potential fluctuations of an option’s value relative to the underlying asset, enabling them to make informed decisions and optimize their trading strategies. This article delves into the intricacies of calculating beta, offering a comprehensive guide for navigating the complex terrain of options trading.

**

Delving into Beta

Beta measures the sensitivity of an option’s price to variations in the price of the underlying asset. It quantifies the extent to which an option’s price fluctuates in relation to the market’s performance. A beta value greater than one indicates that the option’s price is more volatile than the underlying asset, while a beta less than one suggests the option’s price is less volatile. A beta of one signifies that the option’s price moves in tandem with the underlying asset.

**

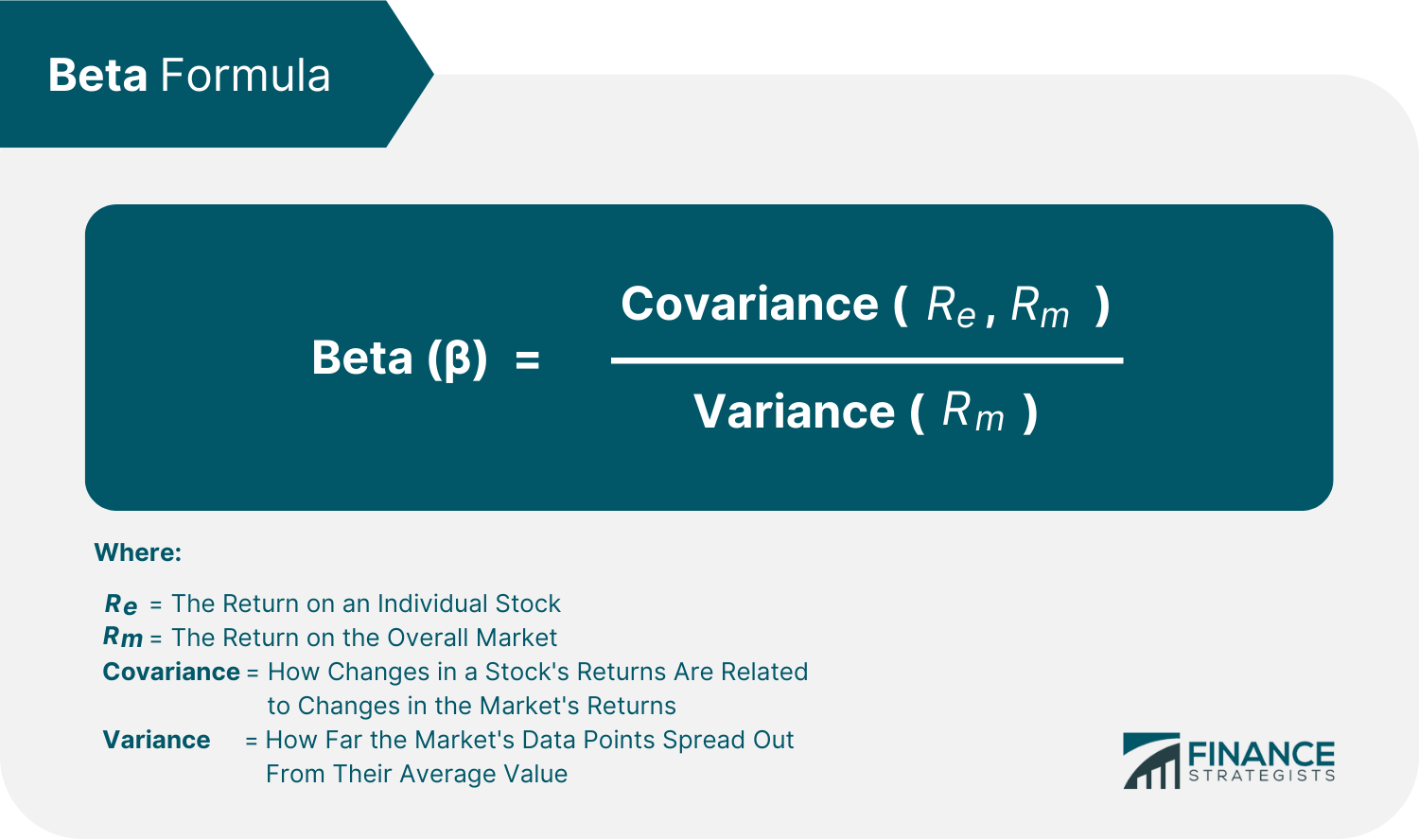

Calculating Beta for Stocks

Calculating beta for stocks is a relatively straightforward process. It involves determining the covariance between the returns of the stock and the broader market, typically represented by a benchmark index such as the S&P 500. The covariance is then divided by the variance of the market index to yield the beta. Specifically, the formula for calculating beta is:

β = Covariance(Stock Returns, Market Returns) / Variance(Market Returns)

**

Image: www.slideshare.net

Calculating Beta for Options

While calculating beta for stocks is relatively straightforward, determining beta for options poses a higher level of complexity. This stems from the fact that options possess a dual nature, being both stocks and derivatives. As such, the calculation involves incorporating aspects of both stock beta and option Greek parameters like delta and gamma.

The formula for calculating beta for options reads as follows:

β = Δ β_Stock + (1-Δ) β_Volatility

Here, Δ represents the delta of the option, β_Stock is the beta of the underlying stock, and β_Volatility refers to the beta of the option’s implied volatility.

**

Additional Considerations

When interpreting beta in options trading, it is essential to consider the following nuances:

- Beta is a historical measure and may not be an accurate predictor of future performance.

- The implied volatility of an option can significantly influence its beta.

- Beta can vary depending on the time to expiration and strike price of the option.

- Beta should be used in conjunction with other analytical tools for a comprehensive assessment.

**

Calculating Beta In Options Trading

Image: www.financestrategists.com

Conclusion

Calculating beta in options trading is a fundamental skill that provides traders with valuable insights into the relationship between an option’s price and the broader market. By leveraging this metric, traders can assess the potential risk and return of an option, and make informed trading decisions. While it is important to note that beta is a historical measure and cannot fully predict future performance, it remains a powerful tool that, when used in conjunction with other indicators, can enhance the decision-making process in options trading.