Image: www.youtube.com

Introduction:

In the labyrinthine world of financial markets, option trading stands as a testament to the human ingenuity to predict and profit from future price movements. And at its heart lies the Black-Scholes model, a groundbreaking formula that revolutionized how options are valued. Embark on a captivating journey as we explore the remarkable history of the Black-Scholes model, unveiling its origins and tracing its indelible impact on the financial landscape.

The Genesis of Black-Scholes:

In the late 1960s, as the financial markets surged with unprecedented fervor, two brilliant minds—Fischer Black and Myron Scholes—envisioned a world where options, once shrouded in uncertainty, could be priced with precision. Inspired by the works of Louis Bachelier, they set out to craft an equation that would unravel the enigmatic nature of these financial instruments.

The Pioneering Equation:

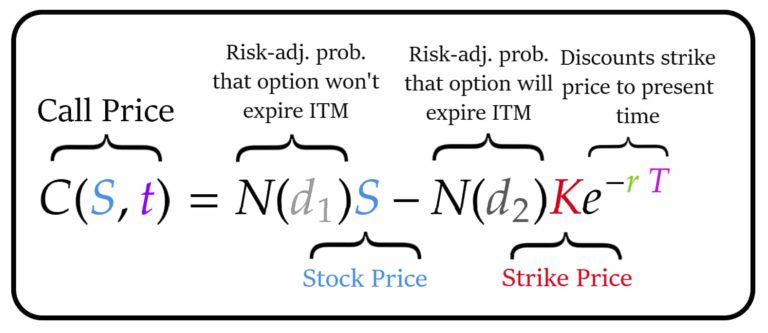

After months of meticulous research, Black and Scholes unveiled their groundbreaking formula in 1973. The Black-Scholes model incorporates a myriad of factors, including the underlying asset’s price, strike price, time to expiration, risk-free interest rate, and volatility. By combining these elements, it assigns a fair value to an option, empowering traders to make informed decisions.

Revolutionizing Option Trading:

The Black-Scholes model rapidly gained ascendancy, becoming the industry standard for option pricing. Prior to its advent, option traders relied on intuition and experience, often leading to substantial losses. However, the formula introduced a level of scientific rigor that transformed the options market. Traders could now price options with greater accuracy, reducing risks and unlocking new opportunities.

The Role of Volatility:

One of the key insights of the Black-Scholes model is its emphasis on volatility. Volatility, a measure of an asset’s price fluctuations, plays a significant role in determining option prices. The higher the volatility, the higher the option value. This understanding empowered traders to capitalize on potential market swings, creating a new era of volatility-based trading strategies.

Evolution and Refinement:

Over the decades, the Black-Scholes model has undergone several iterations to address the limitations of its initial framework. Refinements such as the Barone-Adesi and Whaley models account for factors like stochastic volatility and transaction costs, providing even more accurate pricing. Despite its ongoing evolution, the core principles of the original Black-Scholes model remain steadfast.

Expert Insights and Actionable Tips:

John C. Hull, Professor of Finance, University of Toronto:

“The Black-Scholes model has been a game-changer in the world of finance. It has not only revolutionized option pricing but has also laid the foundation for countless other financial models.”

Actionable Tip:

“Consider using online option pricing calculators that incorporate the Black-Scholes model. These tools can provide instant and accurate price estimates based on the entered parameters.”

Conclusion:

The Black-Scholes model has had a profound impact on the financial world, empowering traders to make more informed and profitable decisions. It has stood the test of time, becoming an indispensable tool for valuing options and unraveling the complexities of market fluctuations. As the markets evolve, the Black-Scholes model will continue to serve as a beacon of precision, illuminating the path toward sound investment strategies.

Image: bradley.bradley.edu

Black Scholes Option Trading History 100000

Image: tradeoptionswithme.com