Introduction:

In the realm of financial markets, options trading presents a dynamic and versatile investment strategy that offers a plethora of possibilities. Central to this strategy is the calculation of option premiums, a pivotal element that sets the stage for informed decision-making. This article aims to delve into the intricacies of options trading premium calculation, unraveling the factors that influence its determination.

Image: www.slideshare.net

Understanding Options Trading Premiums:

An option premium represents the price paid to acquire an options contract. This price is determined by a confluence of factors, encompassing intrinsic value and extrinsic value. Intrinsic value gauges the immediate profitability of an option by measuring the difference between the strike price and the underlying asset price. Extrinsic value, on the other hand, encompasses time premium and volatility premium.

Time Premium:

The time premium captures the value attributed to the remaining time until the options contract expires. As the expiration date draws near, the time premium dwindles,直至最终化为零。通俗来说,时间溢价反映了投资者持有期权合约的时间价值。

Volatility Premium:

Volatility premium accounts for the market’s perception of the volatility of the underlying asset. High volatility indicates rapid price fluctuations, which in turn increases the premium of options contracts. Conversely, low volatility suggests more stable price movements, resulting in lower option premiums.

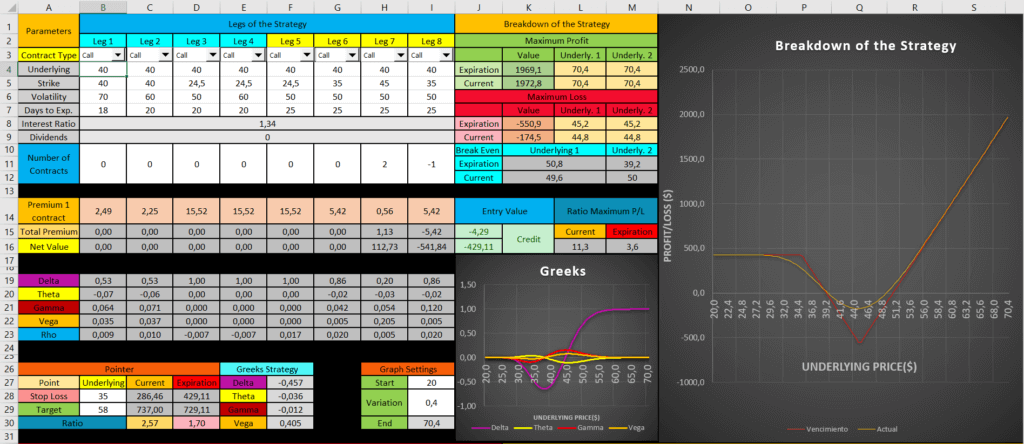

Image: warsoption.com

Factors Influencing Option Premiums:

-

Underlying Asset Price: As the price of the underlying asset moves, so too does the option premium. In the case of call options, an increase in the asset price typically leads to a higher premium.

-

Strike Price: The strike price is the price at which an option holder can exercise their right to buy (in the case of a call option) or sell (in the case of a put option) the underlying asset. Options with more favorable strike prices command higher premiums.

-

Time to Expiration: As mentioned earlier, time premium diminishes as the expiration date approaches. Options with longer time to expiration generally carry higher premiums than those with shorter time horizons.

-

Interest Rates: Interest rate movements impact option premiums by altering the cost of borrowing money. Higher interest rates tend to increase option premiums, while lower interest rates can lead to decreased premiums.

-

Volatility: As previously discussed, higher volatility increases option premiums and vice versa. Market expectations of future price movements play a crucial role in determining the level of volatility premium.

Calculation Methods:

There are various methods for calculating option premiums, including the Black-Scholes-Merton model and the binomial tree model. The Black-Scholes-Merton model, a widely accepted method, employs a closed-form solution to determine option premiums, considering factors such as the underlying asset price, strike price, time to expiration, interest rates, and volatility.

Options Trading Premium Calculation

https://youtube.com/watch?v=TuMCxktgBa8

Conclusion:

Options trading premium calculation is an essential facet of navigating the complexities of options trading strategy. By understanding the factors that influence option premiums and the methods used for their calculation, traders can make informed decisions, mitigate risk, and optimize their overall trading outcomes. This guide has furnished a comprehensive overview of the key elements involved in options trading premium calculation, empowering traders with the knowledge they need to confidently embark on their trading endeavors.