Understanding VIX Weekly Options

The Cboe Volatility Index (VIX) is a real-time market index that measures the market’s expectations of volatility in the S&P 500 index over the next 30 days. VIX options are financial instruments that allow investors to speculate on the future volatility of the VIX index. Unlike VIX futures, which settle in cash, VIX weekly options have physical settlement, meaning that they are settled based on the closing level of the S&P 500 index on the day of expiration.

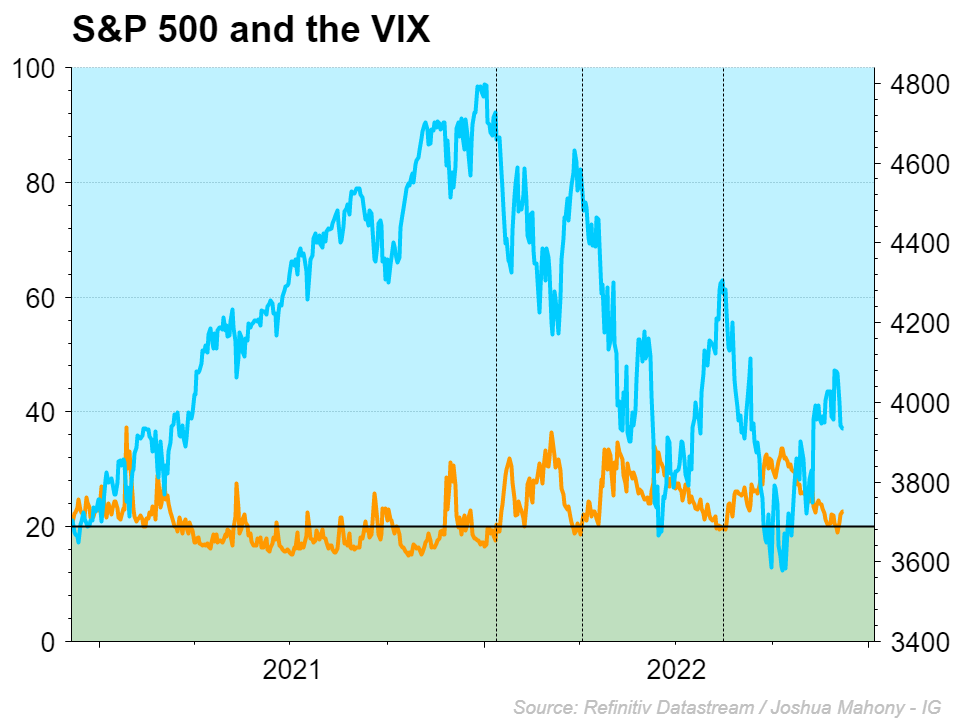

Image: community.ig.com

Settlement Process for VIX Weekly Options

VIX weekly options contracts expire every Friday at 11:00 AM Eastern Time. On the day of expiration, the VIX settlement price is calculated using the settlement formula approved by the Cboe Futures Exchange (CFE). The settlement formula is designed to reflect the average of each strike traded for the best price during an “option auction” settling period on Eurex, held one hour before the option expiration.

Factors Influencing VIX Option Settlement

The settlement price of a VIX weekly option is influenced by several factors, including:

- VIX Index Level: The current level of the VIX index is a primary determinant of option pricing.

- Market Volatility: Market volatility, as measured by the VIX index, affects the implied volatility of options and hence their prices.

- Time to Expiration: The time remaining until expiration has a significant impact on option pricing. The closer to expiration, the lower the time premium.

- Supply and Demand: The number of contracts bought and sold also affects option prices. Higher demand usually leads to higher prices.

Trading Strategies with VIX Weekly Options

VIX weekly options can be used in various trading strategies, such as:

- Long Calls: Buying call options with a VIX strike price above the market is a bullish bet that the VIX will rise.

- Short Calls: Selling call options with a VIX strike price above the market is a bearish bet that the VIX will fall.

- Long Puts: Buying put options with a VIX strike price below the market is a bullish bet that the VIX will fall.

- Short Puts: Selling put options with a VIX strike price below the market is a bearish bet that the VIX will rise.

- Spreads: Combining different types of options with different strikes at different expiration dates can create spreads that limit risk and enhance potential returns.

Image: marketrebellion.com

Risks of Trading VIX Weekly Options

Trading VIX weekly options carries the following risks:

- High Volatility: VIX options are highly sensitive to changes in the underlying volatility of the VIX index.

- Time Decay: The time premium of options erodes over time, especially near expiration.

- Settlement Risk: Physical settlement can introduce additional risks to traders, as the settlement process involves multiple market participants and events.

- Liquidity Risk: VIX weekly options may have lower liquidity compared to other financial instruments.

Trading Vix Weekly Options Settlement

Image: www.makeupera.com

Conclusion

Trading VIX weekly options involves speculative risks and rewards, and traders should carefully consider the risks involved. By understanding the settlement process, factors influencing settlement prices, and trading strategies, investors can effectively manage the risks and pursue potential opportunities in this exciting and dynamic market.

Remember to conduct thorough research and seek professional advice when necessary before engaging in VIX options trading. The Cboe Futures Exchange website, cboe.com/global/vix, provides valuable resources and educational materials on VIX products and their settlement processes.