Option trading is a complex yet potentially lucrative investment strategy that leverages options contracts to speculate on the future price movements of underlying assets. Among the various factors that influence option prices, theta (θ) plays a crucial role in shaping the value of these contracts over time. Theta represents the rate of decay in an option’s value as its expiration date approaches, and understanding its dynamics is essential for successful option trading.

Image: www.youtube.com

Decoding Theta: The Key to Option Time Value

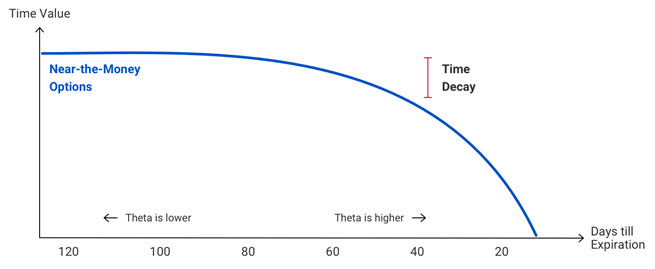

Theta measures the time decay of an option’s premium, which constitutes the intrinsic value and time value components. Intrinsic value reflects the difference between the underlying asset’s current price and the option’s strike price. Time value, on the other hand, represents the market’s expectations about the future price movement of the underlying asset.

As time passes, the time value of an option gradually decays until it reaches zero at expiration. This is because the uncertainty surrounding the future price of the underlying asset diminishes as the expiration date nears, reducing the option’s potential for profit. Theta quantifies this decay, allowing traders to assess the rate at which their options will lose value over time.

The Impact of Theta on Option Strategies

Theta has a profound impact on option trading strategies, particularly those involving options with longer expirations. For instance, in a long call option strategy, the trader anticipates an increase in the underlying asset’s price. If the price fails to rise, the option’s time value will erode rapidly as expiration approaches, potentially resulting in a significant loss for the trader. Conversely, theta can work in favor of option sellers who benefit as time decay reduces the premium they received when selling the options.

Theta vs. Other Option Pricing Factors

While theta is a critical factor in option pricing, it interacts with other variables such as delta, gamma, and vega. Delta measures the sensitivity of an option’s price to changes in the underlying asset’s price, while gamma gauges the change in delta for every unit change in the underlying asset’s price. Vega measures the sensitivity of an option’s price to changes in volatility.

Understanding the interplay between theta and these other factors is crucial for accurate option pricing and effective trading strategies. Traders must consider the combined effects of all these variables to assess the potential profitability and risk associated with any given option trade.

Image: www.youtube.com

Real-World Applications of Option Trading Theta

Theta decay can be leveraged in various option trading strategies to generate income or hedge against risk. One common strategy is theta decay trading, where traders buy an option with a higher time value and sell it closer to expiration when its time value has significantly diminished. This exploits the natural decay process to capture consistent profits.

Theta decay also plays a role in option spreads, where traders combine multiple options contracts with different strike prices and expiration dates. Traders can use spreads to reduce the overall impact of theta decay and enhance their chances of profitability in a given market environment.

Option Trading Theta

Image: mac.x0.com

Stay Ahead with Option Trading Theta

Theta is a dynamic aspect of option trading that profoundly influences the value and behavior of options contracts. By comprehending theta’s influence on option prices, traders can make more informed decisions, develop effective trading strategies, and unlock the full potential of option trading.